The year 2014 marked a pivotal moment for the manufacturing sector, with one term dominating discourse: industrial robots. Driven by rising labor costs, structural industrial adjustments, and a significant reduction in the price of robotic systems, automation witnessed unprecedented growth. The cost of a standard 15kg payload material-handling robot from one of the “Big Four” manufacturers approached a threshold of approximately 200,000 RMB for the robot body alone. While this represents 5-6 times the annual income of an average worker, the economic calculus shifted decisively in favor of automation. An industrial robot can operate 24/7 across three shifts, unaffected by fatigue, without requiring social insurance, housing, or protective gear. With an average operational lifespan exceeding 10 years, the annualized cost—factoring in depreciation and maintenance—falls to around 30,000 to 40,000 RMB. The ability to run continuously makes the actual operational cost of a robot significantly lower than that of human labor, a reality further accelerated by national policies advocating for industrial upgrading.

Industry estimates suggest that China’s installation of industrial robots surpassed 40,000 units in 2014, capturing 20% of the global market and overtaking Japan to become the world’s largest consumer market for industrial robotics. This explosive growth underscores a critical dependency and exposes a core technological gap: the precision RV reducer, the mechanical heart of a robot’s joint.

1. The Technology and Dominance of the RV Reducer

Two primary types of reducers are employed in robotics: the Rotary Vector (RV reducer) and the Harmonic Drive. In articulated robots, the RV reducer is favored for positions requiring high rigidity and rotational accuracy—such as the base, upper arm, and shoulder—due to its superior load-bearing capacity and torsional stiffness. The Harmonic Drive is typically used in the forearm, wrist, or hand.

Japan holds an absolute, monopolistic advantage in high-precision RV reducer technology. Two companies, Nabtesco and Harmonic Drive, command approximately 75% of the global market for precision reducers in robotics. Virtually all leading international robot manufacturers, including ABB, FANUC, and KUKA, rely on these two suppliers for their core drive components. While other players like Germany’s SEW and FLENDER have a presence, and domestic Chinese companies like Shanghai Electric Machinery and Qinchuan Machine Tool have begun R&D efforts, they currently struggle to compete in this high-stakes, precision-critical market.

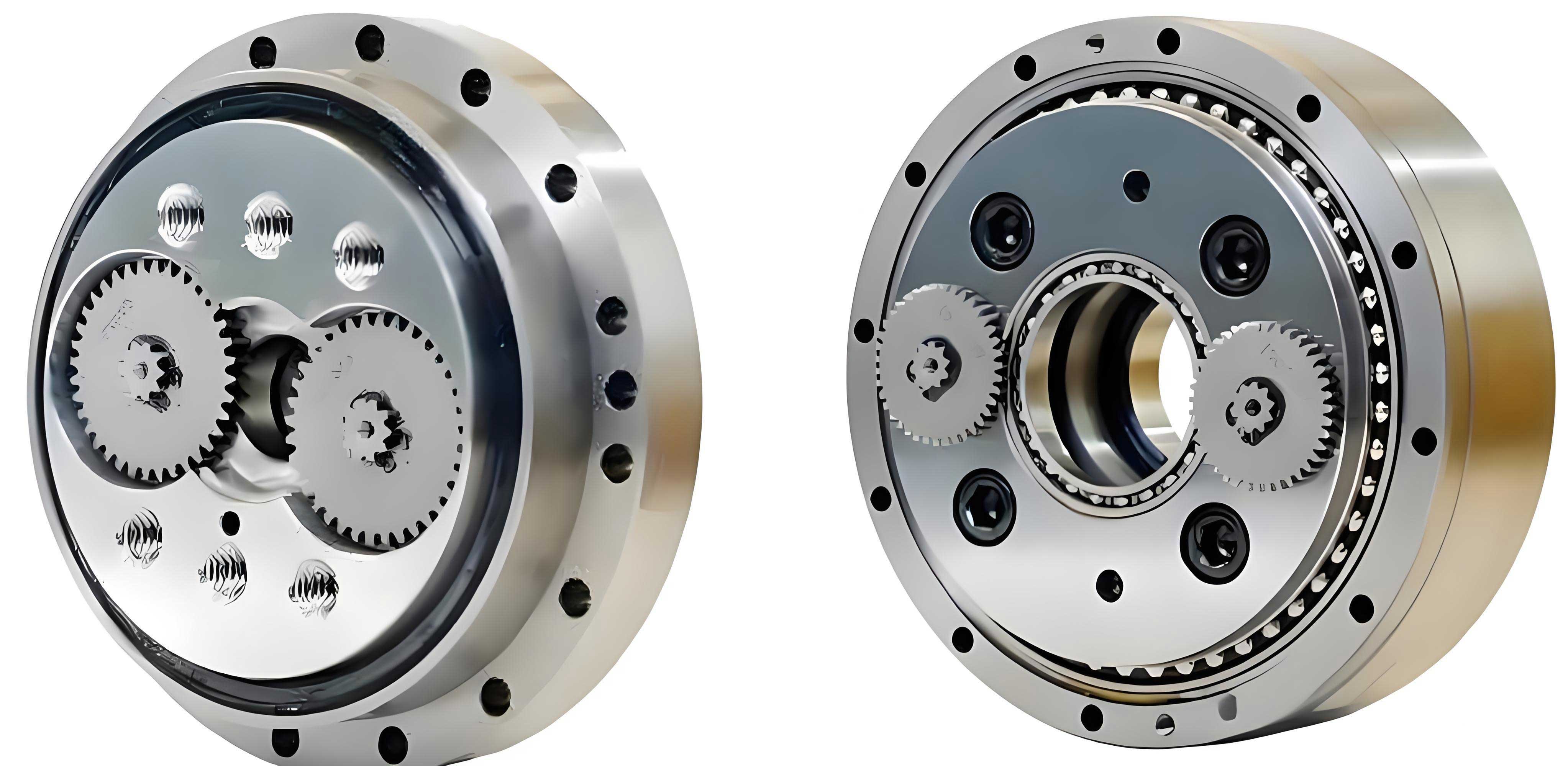

2. Manufacturing Core Components: The Challenge of Precision

The RV reducer operates on a two-stage reduction principle. The first stage is a standard involute gear train. The second, critical stage employs a cycloidal (planetary) pin-wheel mechanism. The input rotation, with high speed and low torque, drives a crankshaft causing eccentric motion. This eccentric motion engages the cycloidal gears (RV gears) with a stationary pin gear housing (ring), converting the eccentric motion into a slow, high-torque rotational output.

The manufacturing bottleneck lies in the ultra-precise machining of two core components: the RV reducer cycloidal gear (RV gear) and the pin gear housing. The profile accuracy of the cycloidal tooth flank is paramount. Deviations in tooth form and flank geometry directly compromise the robot joint’s positional accuracy, operational speed, acceleration capability, and load capacity. This is not a task for universal gear grinding machines, as the cycloidal profile cannot be generated using standard gear hobbing or shaping methods based on involute geometry.

The machining of these parts demands specialized, high-precision form grinding machines. For instance, the MÄGERLE MFP series CNC profile grinding machine is engineered specifically for this task. Its characteristics include a high-power, liquid-cooled grinding spindle motor, a fully automatic wheel balancing system, and a CNC-controlled follow-up coolant system.

The achievable spindle radial runout can be as low as:

$$ \delta_{runout} \leq 0.001 \, \text{mm} $$

Coupled with in-process measurement capabilities, such machines deliver impeccable workpiece geometry and surface finish. The technical specifications and required tolerances for a typical RV reducer cycloidal gear and pin housing can be summarized as follows:

| Component | Critical Parameter | Tolerance / Requirement | Impact on Performance |

|---|---|---|---|

| Cycloidal Gear (RV Gear) | Tooth Profile Error | < 2-3 μm | Backlash, Transmission Error, Efficiency |

| Pitch Accumulated Error | < 5 μm | Motion Smoothness, Vibration | |

| Surface Roughness (Ra) | < 0.2 μm | Wear, Noise, Lifetime | |

| Pin Gear Housing | Pin Hole Position Accuracy | < 3 μm | Meshing Quality, Load Distribution |

| Pin Hole Diameter Consistency | < 2 μm | Preload, Friction, Heat Generation |

The high cost of such equipment—often exceeding 1.2 million USD—reflects the culmination of innovation, specialized process knowledge, and extreme precision. This embodies a manufacturing philosophy centered on “strength through precision” rather than “scale through volume.”

3. Reflections on China’s Precision Machine Tool Industry

The disparity between the specialized grinding machine for RV reducer components and the mainstream output of China’s machine tool industry invites profound reflection. China’s manufacturers have performed a remarkable service by democratizing CNC technology, drastically increasing the domestic数控化率 (numerical control rate) and rapidly closing the knowledge gap with foreign counterparts. However, a fundamental tension exists between the ethos of mass production and the meticulous craft required for world-leading precision.

When production lines are optimized to assemble a CNC lathe every 30 minutes, and a ball screw is mounted in a similar timeframe, one must question whether this represents innovation or a departure from the foundational principles of machine tool building. As one industry veteran aptly noted, the machine tool sector is not akin to the fast-paced IT industry; it thrives on long-term experiential accumulation. The absence of a deep bench of master engineers and technicians possessing tacit “technological know-how” directly impacts the consistency and longevity of precision.

The question then arises: Is the path to “strength” unattainably distant? The answer is a resounding no. Consider two illustrative cases.

A visit to a helicopter engine manufacturer years ago left a lasting impression. Among an array of Swiss precision machines in a temperature-controlled workshop stood a coordinate boring machine produced in the late 1970s by Kunming Machine Tool Plant. The operator noted that after 30 years of service, the machine still held exceptional accuracy, with the original scraping marks on its guideways still visible. Critical components continued to be machined on this veteran tool. This demonstrates that Chinese manufacturers once possessed the capability to build machine tools with exceptional longevity, rooted in mastery of traditional processes like high-quality casting, stress relieving, and hand-scraping—a legacy of deep-seated craftsmanship.

Contrast this with the history of a European grinding machine specialist founded in 1875. Through over a century of industrial revolutions, economic booms, and speculative bubbles in real estate and finance, the company’s leadership remained steadfastly focused on one belief: “We only know how to make machine tools.” Resisting external temptations, they dedicated themselves exclusively to the art and science of precision grinding. Today, they may not be financial titans, but they have perfected their niche. In the fuel injection systems industry, their brand is synonymous with ultimate precision, the default choice for leading global manufacturers.

These narratives highlight a central thesis: achieving excellence is not inherently difficult; the greater challenge lies in mindset. In today’s era of internet-speed expectations and the allure of “quick returns,” the fundamental industrial logic is often overshadowed. The relentless pursuit of immediate “profit” risks the neglect of the foundational “craft.” The core dilemma for China’s precision machine tool sector, and by extension its ability to domestically produce critical components like the RV reducer, can be framed as a strategic choice:

| Paradigm | Core Driver | Primary Metrics | Outcome for RV Reducer Manufacturing | Long-term Sustainability |

|---|---|---|---|---|

| Volume & Scale (“Big”) | Cost Reduction, Market Share | Units Produced, Revenue, Cost per Unit | Enables widespread CNC adoption but fails to produce the ultra-precision needed for core components. | Vulnerable to low-cost competition; lacks technological moat. |

| Precision & Craftsmanship (“Strong”) | Technical Excellence, Niche Dominance | Accuracy, Reliability, Longevity, Process Mastery | Directly enables the manufacturing of RV reducer gears and housings, breaking foreign monopolies. | Builds enduring brand value and technical barriers to entry. |

The economic model for developing a domestic high-precision RV reducer industry is challenging but clear. It requires upfront investment in both R&D and ultra-precision capital equipment (E), sustained over a period (t) before reaching yield (Y). The return, however, is not just in unit sales but in strategic independence and value capture.

Let us define a simplified value capture model. The total cost of a robot joint includes the imported RV reducer cost (C_import), the domestic value-add (V_domestic), and profit margin (P).

$$ \text{Total Joint Value} = C_{import} + V_{domestic} + P $$

Currently, C_import is high and constitutes a large fraction of the joint’s cost. Successful domestic production replaces C_import with a lower domestic manufacturing cost (C_domestic), while potentially increasing V_domestic through advanced machining.

$$ \text{Value Captured Domestically}_{\text{new}} = C_{domestic} + V’_{domestic} + P’ $$

where \( C_{domestic} < C_{import} \) and ideally \( V’_{domestic} > V_{domestic} \). The national and industrial benefit (B) can be expressed as the reduction in import dependency plus the increase in high-value manufacturing capability:

$$ B \approx (C_{import} – C_{domestic}) + \alpha (V’_{domestic} – V_{domestic}) $$

where \( \alpha \) is a multiplier representing the strategic value of technological sovereignty. The barrier is the initial investment I in precision machine tools and process development, which must be amortized over the production volume N:

$$ \text{Break-even requires: } N \cdot (C_{import} – C_{domestic}) > I $$

Given the projected growth of the Chinese robotics market (N is large and growing), this equation eventually favors investment. The real challenge is the patience and focus required during the period where I is being expended and yield is low.

In conclusion, the journey towards mastering the RV reducer is a microcosm of China’s broader aspiration to transition from a manufacturing giant to a manufacturing powerhouse. It is a path that cannot be shortcut by volume alone. It demands a renewed reverence for cumulative experience, a dedication to specialized craftsmanship, and the strategic patience to cultivate deep technological roots. The machines that build the core of advanced robotics are themselves products of this philosophy. The choice between “big” and “strong” is ultimately a choice between fleeting advantage and enduring capability. For the future of China’s precision manufacturing, embracing the latter is not just an option; it is an imperative. The development of a robust domestic RV reducer supply chain will serve as a key indicator of progress on this challenging but essential path.